Editor's Note: A portion of these results appeared in our November/December issue, but we wanted to be sure you had access to all of the information, especially that which could not fit in the printed issue. We hope you enjoy this peek into one of the most popular sessions at the PARCEL Forum, and we hope to see you there next year, September 18-20, in Nashville! Visit www.PARCELForum.com for more information.

We asked the questions, you provided responses. For the fourth consecutive year at the PARCEL Forum, Shipware, LLC conducted a live parcel pricing and benchmarking survey in which 56 shippers responded to survey questions about their parcel usage, carrier preferences, cost reduction strategies and other valuable benchmarking data. Survey respondents collectively commanded approximately $2 billion in annual parcel spend.

Contracts were not shared, but rather, participating shippers responded anonymously to survey questions based on ranges. Technology-enabled and totally blinded to avoid confidentiality concerns, the survey was designed to help shippers to better understand how their pricing stacks up with other shippers. Moreover, all survey responses were cross-tabulated by industry, company revenues, primary carrier, and annual parcel volume/spend for more meaningful like-volume correlations.

Why is benchmarking parcel pricing data so critical? Well, the most common challenge I hear from volume parcel shippers is that they don’t know how good – or bad – are the incentives, terms and structure of their carrier pricing agreements. While no shipper would ever negotiate a contract and knowingly leave money on the table, the reality is that some shippers have clearly done a better job than others when it comes to negotiating the most favorable rates and terms.

Published for the first time to non-survey participants, this article provides survey results on general parcel procurement, general rate increases, strategies to mitigate rising costs and receptivity to US Postal Service parcel products as a compliment to the services of the private national carriers, and more.

SURVEY DEMOGRAPHICS

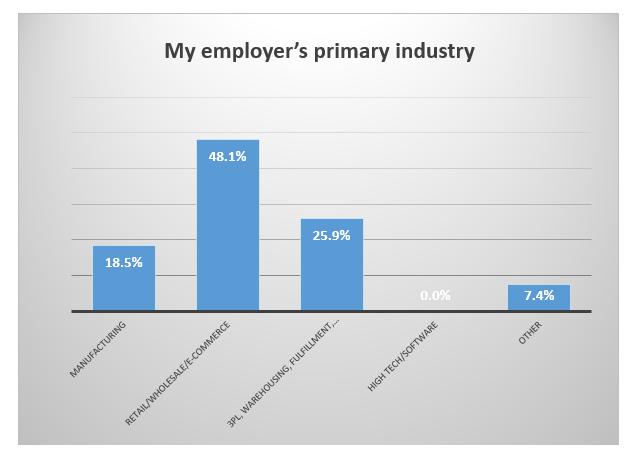

Industry

While participants included a mix between several industries the most common sector was retail/wholesale/ecommerce followed by 3PL/warehousing/fulfillment and manufacturing.

Annual Revenues

Small and large companies alike were represented with annual sales revenues ranging from under $100M to those businesses that generate revenues greater than $10B.

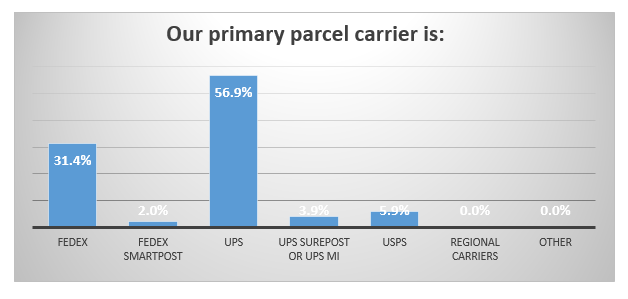

Primary Carrier

Predictably, 95.1% of all survey participants named UPS or FedEx as the “primary” carriers (as defined as more than half of overall volume). Other carriers included USPS and regional carriers although adoption of carriers outside of FedEx and UPS was not common.

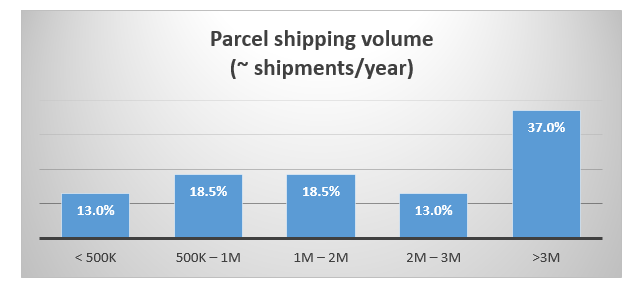

Parcel Volume

Annual parcel volume revealed a balanced mix of small, medium, large and mega shippers, although as expected for the PARCEL Forum audience, half the survey participants shipped high volumes of more than 2 million parcels annually.

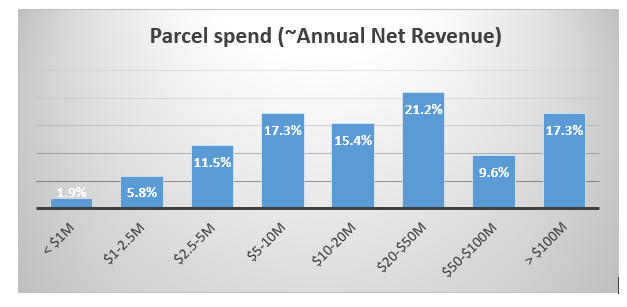

Parcel Spend

Annual parcel expenditures likewise revealed a balanced mix of shippers of all sizes. Collectively, Shipware estimated survey participants command annual parcel spend of $2 billion.

GENERAL PARCEL PROCUREMENT

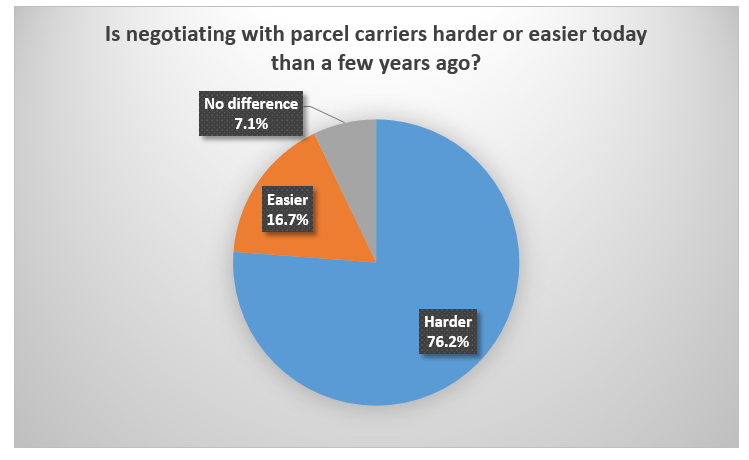

By a margin of 4.5 to 1, survey respondents feel carrier negotiations have become harder rather than easier over the years.

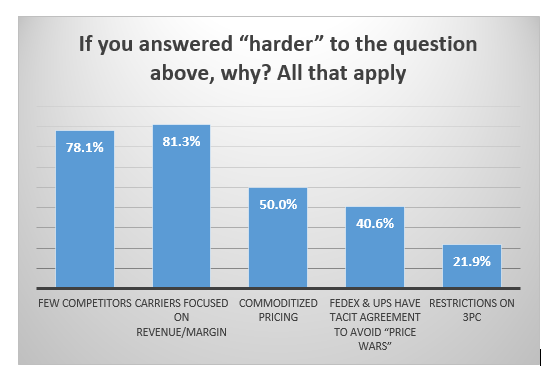

We followed up asking those shippers that feel it’s harder than ever to negotiate pricing with the major national carriers to explain their answer. Primarily, shippers believe it’s due to the fact that the carriers are focused on operating margins (81.3%), hence tougher pricing negotiations. Others believe it’s because the industry has few national, private carrier options to FedEx and UPS (78.1%), and that pricing has become more of a “commodity” with pricing so closely aligned between the two rivals (50.0%).

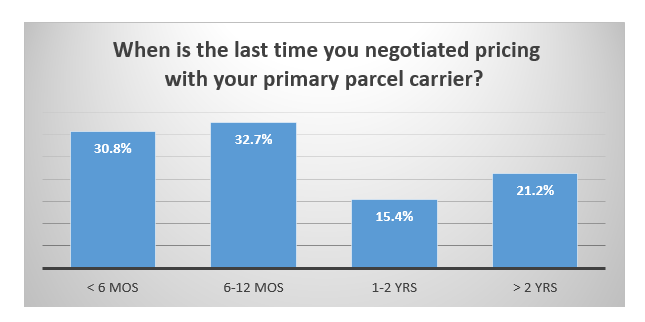

Shippers and carriers were busy making pricing changes in 2016. 63.5% negotiated pricing with their primary parcel carrier within the last 12 months. By further correlating actual pricing results mapped to the frequency of negotiations, the data would suggest that those companies having negotiated contracts more recently are in fact driving deeper discounts than those shippers that hadn’t negotiated in more than 2 years.

Shipware advocates that shippers should create an expectation with carrier reps of ongoing cost reduction. Notable reasons to bring the carriers back to the negotiation table include changes in shipping profile: volume fluctuation, changes in shipping product utilization, zonal distribution shifts, weight/DIM changes, etc. Moreover, changes in FedEx Earned Discounts thresholds and UPS Portfolio Tier changes, up or down, are legitimate reasons to make contract changes.

However, the most effective rationale for initiating pricing improvements with FedEx and UPS are changes in the market place. The rise of the USPS as a legitimate third option – especially when comparing Priority Mail to Ground – regional parcel carrier options, package consolidators and parcel select players, service guide and pricing changes initiated by FedEx and UPS, etc.

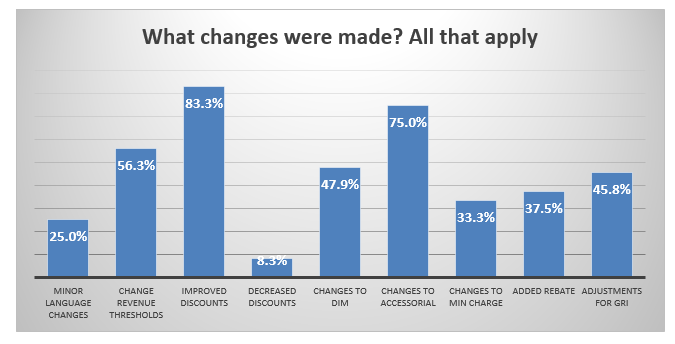

We followed up by asking what changes were made during the most recent negotiations. Most popular responses were discount improvements (83.3%), contract changes related to accessorial charges (75.0%), revenue threshold changes (56.3%) and adjustments to address General Rate Increases (45.8%).

It is important to note that what’s meaningful for one shipper may not be meaningful for another. It is important to conduct a comprehensive analysis to understand which pricing contract changes will have the most material impact.

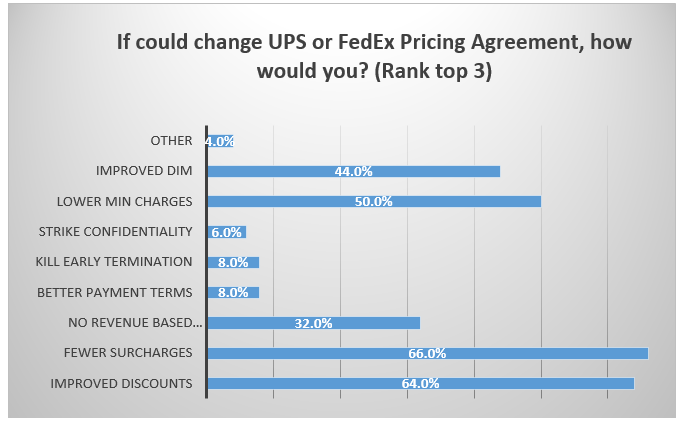

When asked to rank the top three ways shippers would change their UPS and FedEx pricing agreements, minimizing surcharges was the highest weighted response (66.0%), amazingly higher than getting deeper discounts (64.0%). Shippers would also like to lower minimum charges (50.0%) and have more favorable DIM factors/thresholds (44.0%).

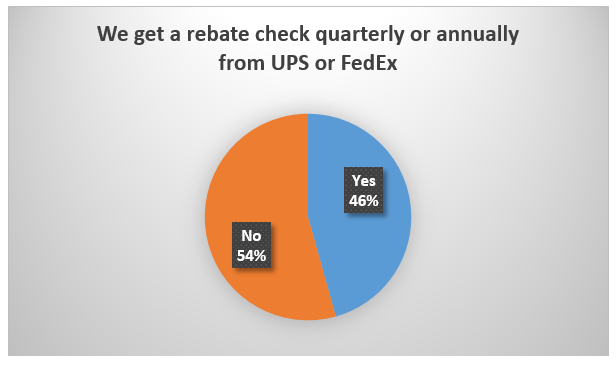

While historically a UPS discounting vehicle (deferred rebates), FedEx is also offering rebates. Called FedEx Earned Discount Override Program, select shippers who receive rebates get monthly, quarterly or annual rebate checks for meeting negotiated revenue thresholds. Rebates are quickly becoming a popular carrier incentive. 46% of survey participants now get rebate checks from either UPS or FedEx.

There are pros and cons of rebates. In general, Shipware does not advocate rebates. Rebates are one of many forms of carrier retention tools designed to keep shippers locked into using their services only. Plus, the carrier hangs onto your money for a specific time period (in some cases, one full year). Not good for those companies that need working capital. Rather, we prefer to see the carrier give those discounts to shippers upfront, rather than “earn back” dollars through rebating.

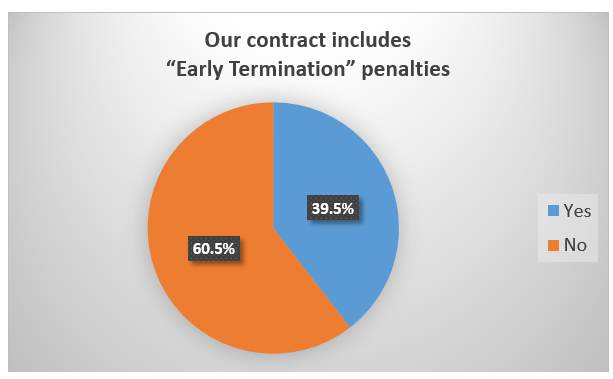

Unfortunately for shippers, one-sided contract language including Early Termination Agreements (ETAs) – essentially, financial penalties for terminating parcel contracts prior to its renewal date – are becoming more common with more than one-third (39.5%) of shippers reporting their contracts include ETAs

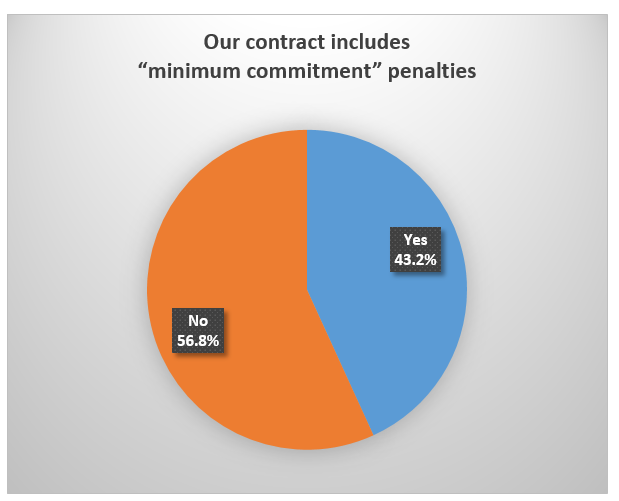

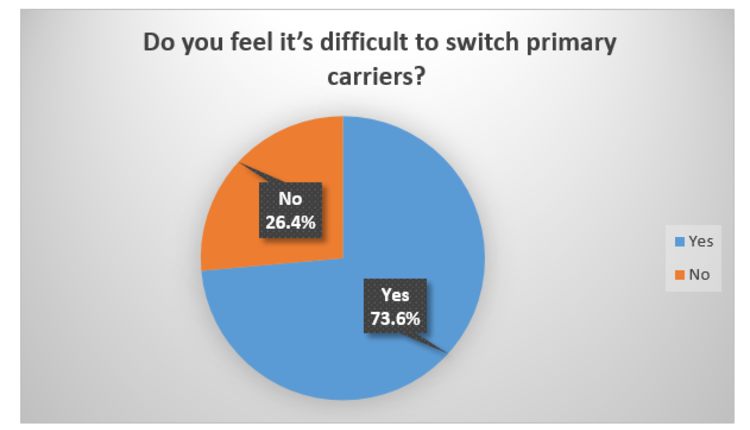

Carrier retention strategies like rebates, ETAs, minimum commitments and many others have been extremely effective in UPS and FedEx’s ability to maintain long term customer relationships despite an extremely competitive industry. In fact, nearly three quarters of shippers (73.6%) feel it would be very difficult to switch their primary carriers.

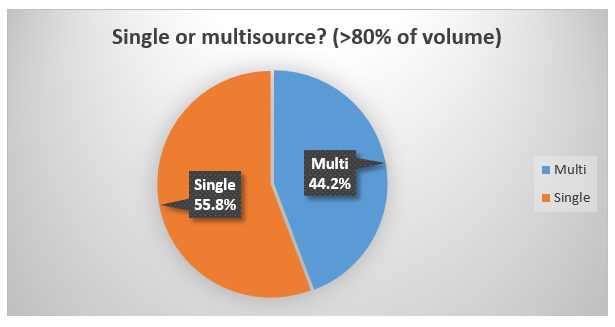

These retention strategies contribute to the fact that the majority (55.8%) of shippers surveyed single source (as defined as 80% or more volume going to a single carrier).

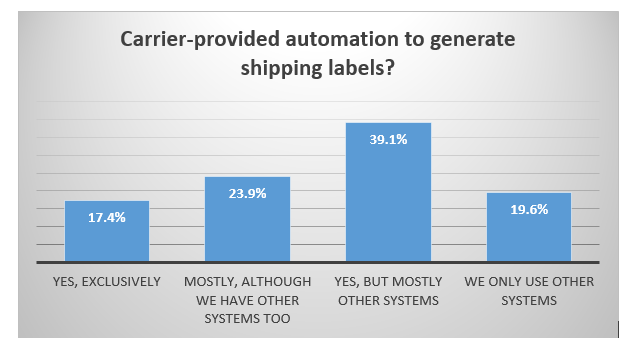

Despite these results, it is surprising that less than half of shippers exclusively (17.4%) or mostly (23.9%) use carrier-provided automation to create shipping labels. The remaining 58.7% mostly or exclusively use manifesting systems that enable greater choice and flexibility in carrier selection.

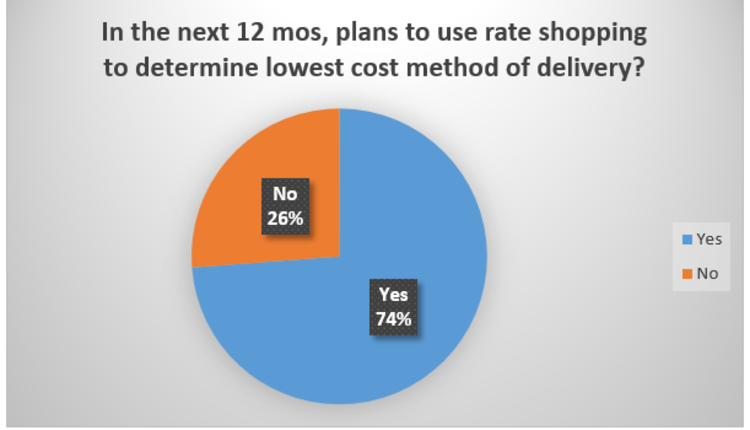

And shippers are continuing the move to greater flexibility and carrier choice, with nearly three quarters reporting that they concurrently or plan within the next year to use rate shopping tools for least-cost, best-way package routing between multiple carriers.

Everyone knows that FedEx and UPS offer package delivery by defined and guaranteed transit times or your money back, right? Yes, but only if you haven’t waived your right to file service claims, which half of our survey audience has done.

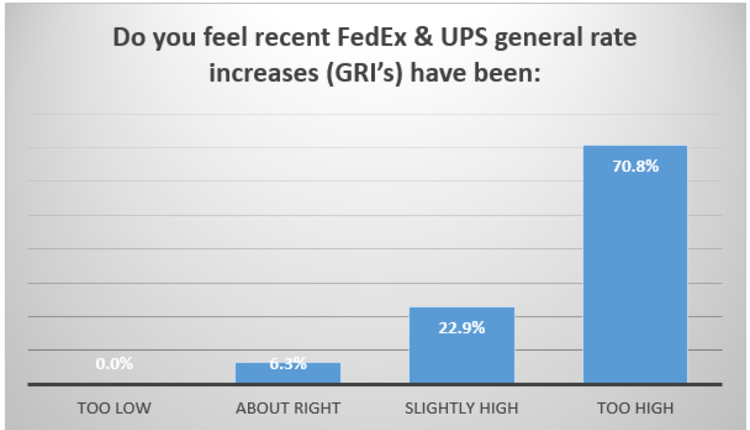

Most shippers expressed concern about recent carrier General Rate Increases (GRI’s) with 93.7% feeling the increases have been “slightly” or “too high”.

GENERAL RATE INCREASES AND COST MITIGATION STRATEGIES.

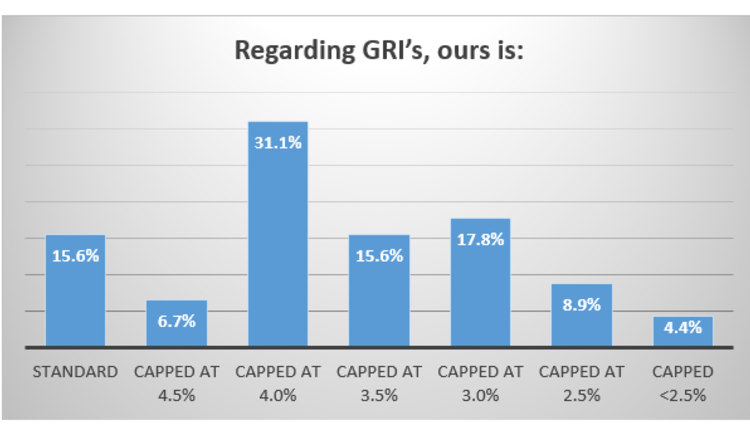

Even amongst the survey group’s $2 billion in collective parcel spend, 15.6% continue to receive the standard/published General Rate Increase (GRI). For those shippers that negotiated a “cap” to the GRI, 64.5% are capped between 3-4%. Only 4.4% of shippers have a GRI cap of 2.5% or less.

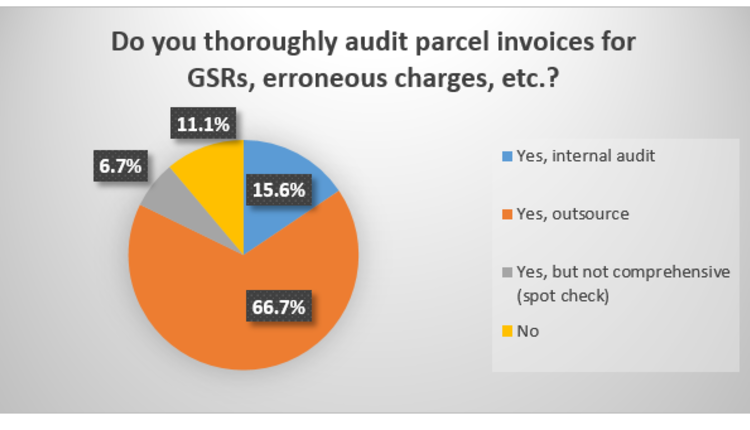

To mitigate rising shipping costs over the past year, shippers have tried many strategies including rate negotiations (72.0%), auditing carrier invoices (66.0%), improving packaging to minimize empty fill space and dimensional charges (50.%), and greater use of the US Postal Service, regionals and other alternative carriers.

While many of these strategies will continue over the next year, shippers expressed significant increases in many areas, especially using least cost routing software, intensifying the use of the US Postal Service and regionals, zone skipping, continuing to optimize packaging, and focusing on the cost of returns.

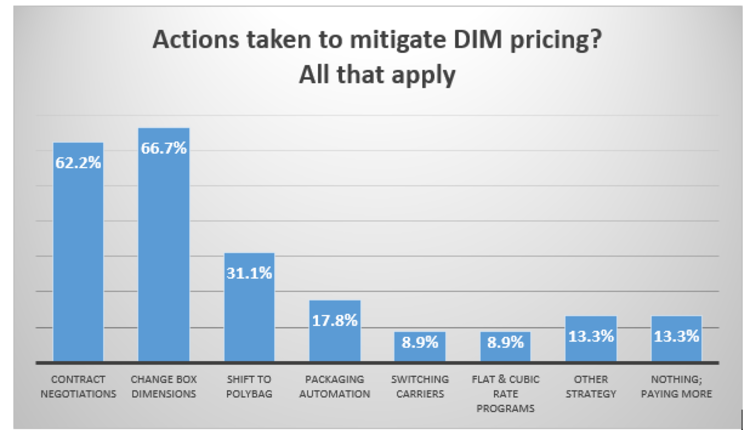

Specific to mitigating higher costs associated with dimensional pricing, shippers are changing box sizes (66.7%), negotiating specific dimension based contract concessions (62.2%), shifting from corrugated to polybags for some shipments, and looking to packaging automation (17.8%). Surprisingly, fully 13.3% of PARCEL Forum shippers surveyed do not plan on taking further action related to dimensional pricing.

U.S. POSTAL SERVICE

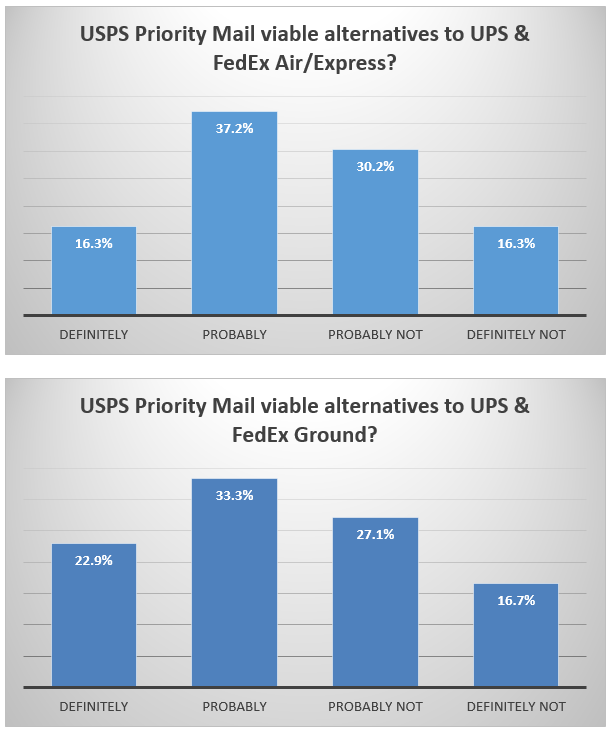

The last part of our survey recap addresses shippers’ attitudes about the US Postal Service. Comparing survey responses from previous years, shippers are categorically becoming more comfortable with the US Postal Service as – if not a replacement – certainly a viable alternative or compliment to FedEx and UPS services. 53.5% of respondents feel USPS Priority Mail is “probably” or “definitely” a viable alternative to FedEx and UPS Air services. The number increases to 56.2% when comparing Priority Mail to Ground services.

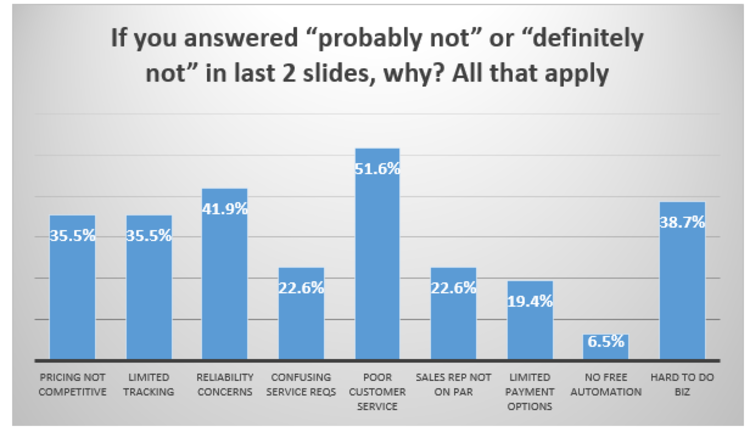

Despite the increases over the years, still nearly have of shippers believe the Postal Service is “probably not” or “definitely not” a viable alternative for either Air or Ground services. Reasons cited included poor customer service (51.6%), reliability concerns (41.9%), difficult to do business with the USPS (38.7%), limited tracking (35.5%) and uncompetitive pricing (35.5%) amongst other negative perceptions.

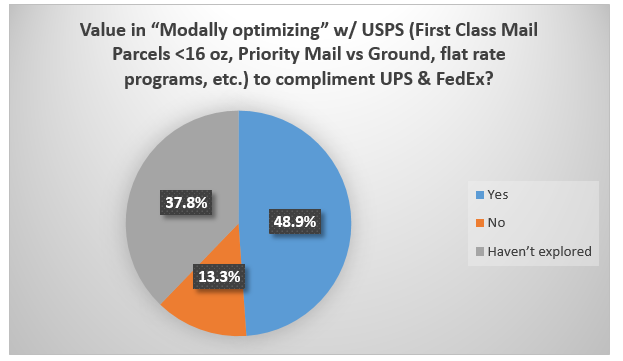

Despite the ongoing – but decreasing – negative perceptions, the Postal Service certainly offers an opportunity for shippers to compare services and pricing. Nearly half of shippers (48.9%) believe they could benefit with faster delivery transit and reduced costs through USPS modal optimization for some packages as a compliment to FedEx and UPS national services. While only 13.3% disagree, 37.8% of shippers just haven’t yet gotten around to exploring USPS opportunities.

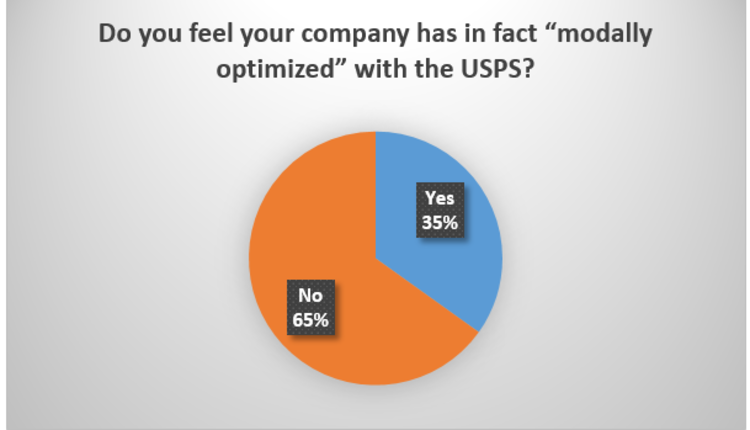

Therefore, not surprisingly, 65% of shippers do not yet feel their distribution is modally optimized to include all USPS product offerings.

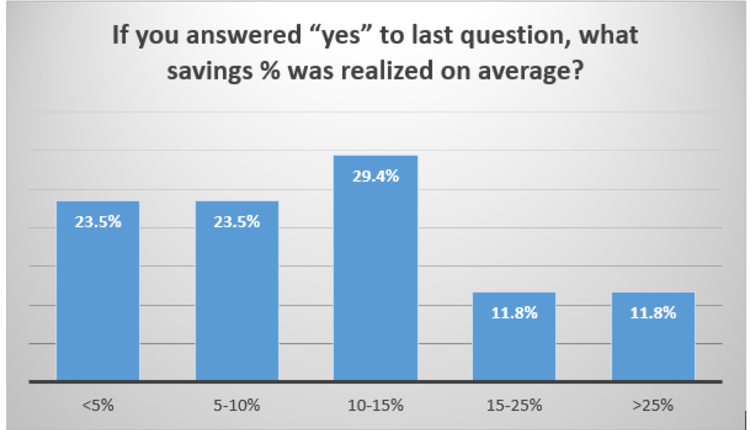

As a follow up, we asked the 35% of shippers who claim to be optimized with the Postal Service to report savings achieved. 76.5% report savings greater than 5%, with nearly one quarter (23.6%) experiencing savings greater than 15%.

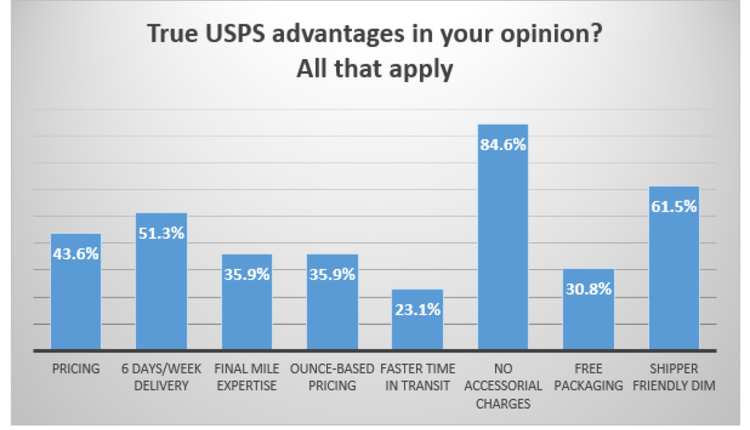

We asked the audience to list true advantages of the Postal Service. Most popular responses included no accessorial charges (84.6%), shipper friend dimensional pricing (61.5%), 6 day/week delivery (51.3%), competitive pricing (43.6%), ounce-based pricing (35.9%), final mile expertise (35.9%), free packaging (30.8%) and faster transit times (23.1%).

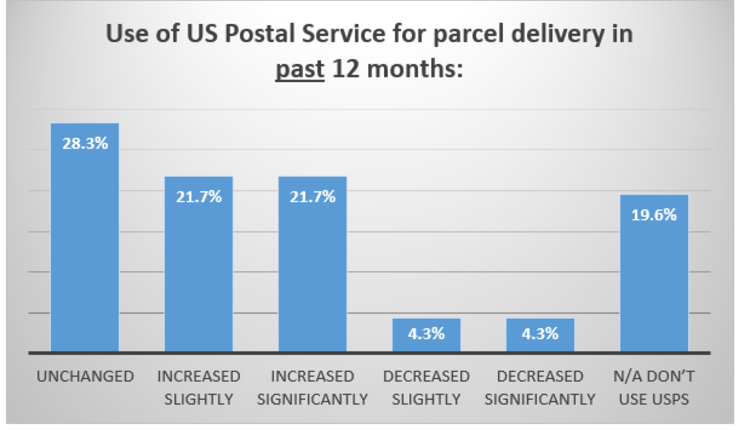

While 28.3% of shippers reporting their use of the USPS to be unchanged over the past year, 43.4% increased “slightly” or “significantly”. Only 8.6% decreased use of the US Postal Service.

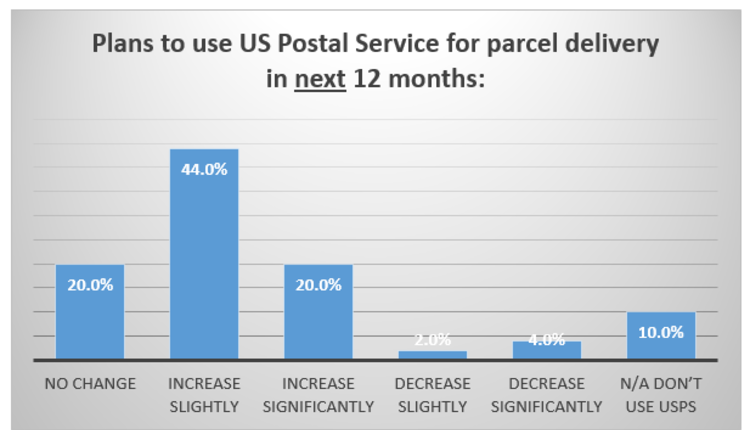

And the future looks bright for the Postal Service as 64% of shippers intend to slightly or significantly increase use of its services over the next 12 months.

Of course, benchmarks can only take a shipper so far in their carrier negotiations. While overall volume and revenue certainly play a role in pricing, FedEx and UPS discounts are largely based on the carriers’ analysis of distribution footprints and physical package characteristics, which are directly tied to the carrier cost drivers. Other pricing factors include desired carrier operating ratios, sales commissions, strategic account value, and competitive considerations.

Therefore, simply reviewing benchmarking data may not be enough to draw conclusions that you, too, should be receiving similar discounts. Benchmarks like those published above will provide shippers with an idea of what’s possible – high watermarks for which to strive. Finally, when survey questions are cross-tabulated with shipper volume, spend, industry or other key metrics, shippers are better able to correlate their results with more relevant peers.

Rob Martinez, DLP is President & CEO of Shipware LLC, an innovative parcel audit and consulting firm that helps volume parcel shippers reduce shipping costs 10%-30%. Rob offers more than 25 years’ experience negotiating parcel contracts – on both sides of the negotiating table – for some of the most recognizable brands in the world, and is a sought after speaker and industry thought leader. He welcomes questions and comments, and can be reached at 858-879-2020 Ext 114 or rob@shipware.com.