Editor's Note: This article was written in fall of 2023, but even though this most recent peak season is now over, we still thought this article from our November/December issue should be shared, since it's never too early to start preparing for next year!

Guiding your peak season strategy requires knowledge of carrier tendencies. Periodically, carriers introduce a new charge or implement new ways of calculating cost to shippers, leading to significant shifts in pricing dynamics. Some of these changes are permanent, such as dimensional weights, remote area surcharges, and large package and overmax fees. Others, initially perceived as temporary, over time become permanent — like the peak surcharges, now rebranded as demand surcharges.

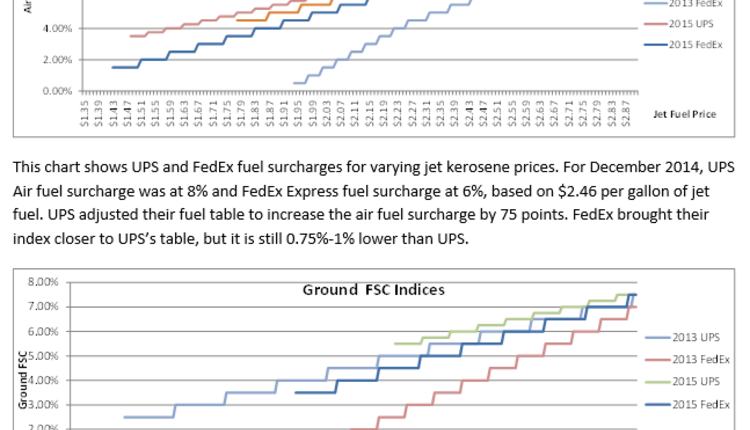

When COVID-19 impacted the market in 2019-2020, the sales shift from brick-and-mortar stores to online marketplaces dramatically accelerated, causing a huge demand spike on the parcel carriers. At that point, a peak surcharge was arguably justifiable, and carriers implemented different surcharges for residential, oversized, and international packages. Three years later, however, that demand has dissipated. Carriers are left with extra capacity built during the peak period, yet shippers incur peak/ demand surcharges that apply year-round. From January to October, a milder set of surcharges are applied to residential and oversized packages, and from October to January, they increase based on a complex calendar and methodology.

There are a multitude of approaches that shippers can employ to tackle the holiday peaks:

Create your own peak: Demand Surcharges are most expensive from October to January. One strategy that a retailer can employ is to drive the sales to mid-summer through incentives and sales campaigns. Carriers use June/July volumes as a baseline while calculating the peaking factor. Increasing the baseline will help reduce the peaking factor during the holiday season.

Get closer to your customers for oversized and long zone packages: Carriers are penalizing large/ oversize/overweight boxes, and the surcharges are more expensive for higher zones. What’s worse is that the annual rate increases have been hitting the higher zones more in recent years, including with the 2024 GRI. If your operation has multiple DCs, make sure to stock the large SKUs in all DCs and fulfill from the closest warehouse. If ship-to-store is an option, incentivize buy online, pickup in store (BOPIS) for larger boxes. Finally, look for 3PLs that are willing to deliver those large boxes without charging hundreds of dollars in surcharges. This will allow you to place the SKUs closer to your customer, reducing the cost and transit time.

Add USPS to the carrier mix: USPS is the largest parcel carrier in the US, and its recently introduced Ground Advantage service offers competitive pricing. USPS also announced that it won’t charge any peak surcharges in 2023. Moving some of the non-time-critical shipments to USPS will reduce the peaking factor for UPS and FedEx, resulting in savings from multiple avenues. We have seen sporadic operational challenges with shippers who switched recently to the Ground Advantage, and it is yet to be seen how this service performs during the 2023 peak; however, we believe USPS should be considered a viable addition to most mid to large-size shippers.

Negotiate better discounts for your program: Carriers have extra capacity thanks to USPS, Amazon, and the regional carriers. UPS has lost shippers during the Teamster negotiation uncertainty, further increasing its capacity. According to FreightWaves Pricing Power index, the shippers have the upper hand at the negotiation table. Both UPS and FedEx announced 5.9% GRIs for 2024, but the accessorials and peak surcharges are going up at higher rates than the 5.9%. Shippers should be able to negotiate some of these charges to reduce the burden of increased cost during the peak season.

In summary, the key to a successful peak season lies in understanding the primary drivers of your parcel costs, necessitating a comprehensive grasp of your parcel data. Additionally, readiness to add or switch carriers or 3PL providers when necessary is crucial. Shippers currently hold significant negotiating power, and should capitalize on the current economic landscape to mitigate shipping costs effectively.

Baris Tasdelen is Manager at Körber Supply Chain. He can be reached at baris.tasdelen@koerber-supplychain.com.

This article originally was published in the November/December, 2023 issue.